Despite being in the crystal down cycle in November, the consolidated sales revenue in the LCD sector from the 4 major Taiwan panel makers still reached NTD 78.504 billion, a 1.4% increase MoM and also an increase of 1.4% during the same period of last year. The aggregate large-sized panel shipments in November were up by 6.0% to 18.91 million units; compared to last year, the figure rose by 101.2%.

Taiwan Sales performance

Of the 1.4% consolidated revenue growth, only CMO and CPT showed positive growth. For CPT, in addition to the ease of glass shortage, order increase after the CMO-Innolux merger further drives its MoM shipment growth of large-sized and small-sized products by 26.9% and 29.1% respectively, with monitor shipments growing more significantly. CPT’s outstanding shipment performance generated a 9.2% MoM revenue growth to 5.8 billion. On the other hand, CMO benefitted from China’s domestic demand, its monitor and TV shipments increases by nearly 10% each, generating an 8.7% growth in consolidated revenue of 29.9 billion. The other panel makers were impacted by the crystal down cycle, AUO’s revenue declined by 3.0% to 38.4 billion, and HSD fell by 12.0% to 4.4 billion.

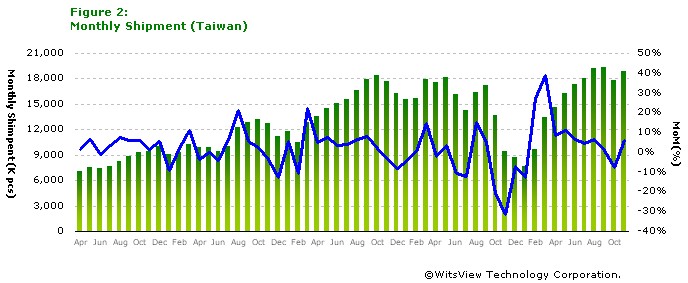

Taiwan Shipment

Shipment-wise, the 4 major Taiwan panel makers posted an increase in the slow season, especially CPT, which posted the biggest growth, where it rose by 26.9% MoM to 1.65 million units. Meanwhile, AUO, CMO were up by 4.5% and 5.1% MoM to 9.32 million and 7.07 million units respectively. HSD was the only one that declined, down by 3.7% to 867 thousand units.

More detailed analysis is provided to WitsView Intelligence members. Interested in being Intelligence members? Contact us! mkt@witsview.com