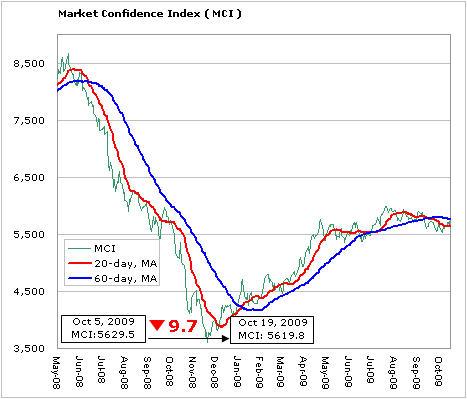

Between October 5th and 19th, MCI index slipped 9.7 points from 5629.5 to 5619.8. The index continued to hover between 5600 and 5700 points, ending in a minor fall. Last week, LGD was the first to announce its third quarter financial results, recording a 15% QoQ revenue growth; and this week, several global panel makers will also be releasing their third-quarter financial results, which are expected drive up their respective stock prices in the short-term. Outlook for the fourth quarter – as MCI is currently at a low level, it indicates that future economic outlook will continue to be fairly conservative, although China’s National Holiday sales performance was in line with market expectations, and consequently eased the issue of inventory build-up. Furthermore, because panel shipments have already peaked in September/October, brand vendors are gradually lowering their orders, which results in a continued decline in panel prices, a sign that panel prices have reached a turning point; subsequently, sales performance during Christmas holidays and traditional festivals will be a key focus of panel makers.

More detailed analysis is provided to WitsView Intelligence members. Interested in being Intelligence members? Contact us! mkt@witsview.com