With May 1st Golden Week Coming, Panel Makers’ Restocking Momentum Remains, Market Confidence Flat

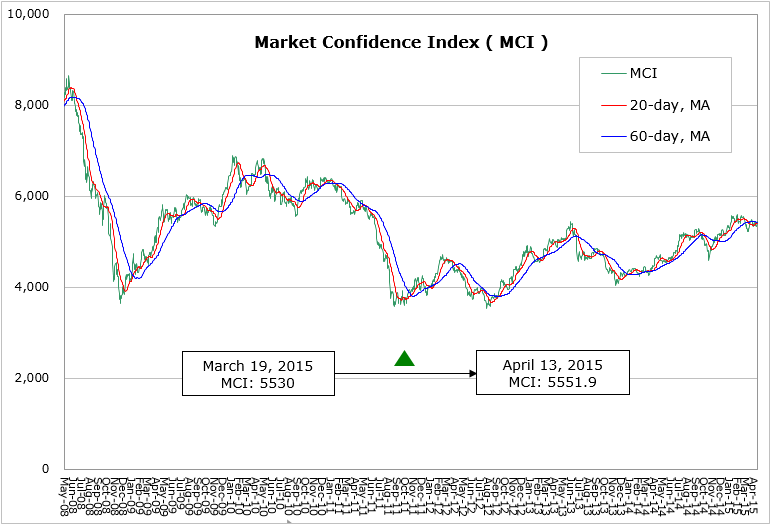

According to the latest data by WitsView, MCI climbed by 21.9 points from 5530 to 5551.9 points from Mar. 19 to Apr. 13 2015. The weak U.S. economic figure results in the soft U.S. dollar. The nation’s Commercial Department revealed GDP growth 2.2% for the last quarter of 2014, which is lower than expected. The manufacturing and service PMI published by ISM both declined to 51.5 and 56.5. The Fed holds off the decision to lift interest rate, while central bank officials show divergence over the timing of interest rate hike, based on the meeting minute of FMOC, as there is still doubt over the stable U.S. economic recovery. The European QE performs initial effectiveness as the unemployment rate reached the new low for three years and the composite PMI in March attained the 11-month high 54.0. Greece is in the negotiation with EU to solve the debt crisis as it makes concession on implementing the bailout condition. However, the details remain unclear and the South European country attempts to seek support from Russia to balance EU’s influence, adding economic uncertainties to the euro zone.

AIIB (Asian Infrastructure Investment Bank) initiated by China gains members including European countries, Korean, and emerging countries Russia, and Brazil after the U.K. joining in March as the first European member. The development of AIIB will be a main indicator to the power balance between China and the U.S. The Chinese government continues to support the economic growth in other aspects on top of the quantitative easing policy, and as the framework of “One Belt and One Road” is announced, the excessive capacity is likely to be digested with the international infrastructure projects and development partnership among the eastern and the western countries. Bank of Japan sticks to its plan of purchasing debts equivalent to JPY 80 trillion annually, and the reduction of the debt purchase program is unlikely until the 2% inflation rate target is reached and the economy shows significant growth. The monetary policy sees possibility to ease further in Q2. To sum up, the U.S. economy cools down, the euro zone has signs of recovery, China attempts to stir economy with regional integration strategy, and Japan waits patiently for the growth.

As we are in Q2, the sales during May 1st holidays comes under the spot light. As brands have demand for restocking, and the holidays see restocking momentum to a certain degree, the panel demand stabilizes in April in China. However, WitsView expects the sales during Labor Day holidays to decrease 4-5% YoY, and the panel demand is likely to weaken significantly from May. Based on WitsView’s latest panel price survey, the TV panels develop toward large sizes, which helps digest capacity. Nevertheless, Chinese brands hold a conservative view on the demand during May 1st holidays and adjust the procurement volume, dragging down prices of most TV panel sizes. The IT panel price will probably continue to drop through the end of Q2 with the demand seeing no sign of recovery and elevated inventory. The new competition of panel equipment investment starts to heat up. Even with three G8.5 fabs beginning operation and other fabs being ready in 2016, Chinese and Korean pane makers plan to invest in large generations including G9.7 and even G10.5. With the government’s strong support, Chinese panel makers race for the leading places as the winners in the market are relied on the ample capital to build up equipment. Chinese panel makers in 2015 are likely to ramp up more investment than Taiwanese and Korean rivals.

More detailed analysis is provided to WitsView Intelligence members. Interested in being Intelligence members? Contact us! mkt@witsview.com