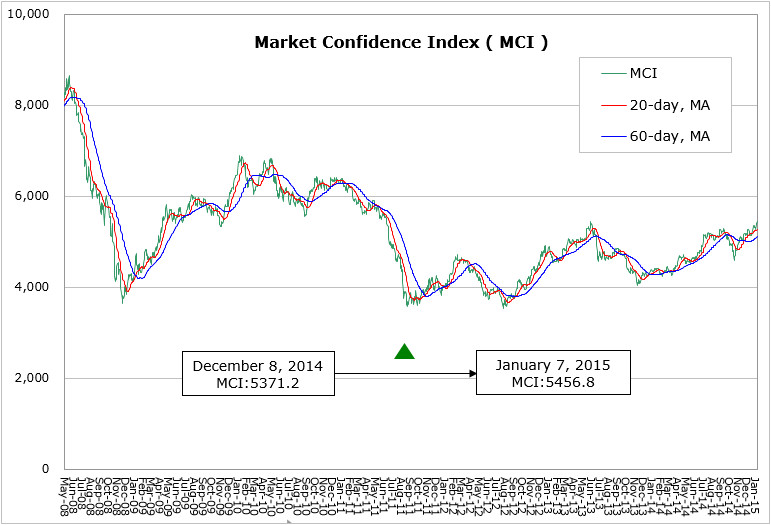

According to the latest data by WitsView, MCI climbed 85.6 points from 5371.2 points to 5456.8 points from Dec. 8th 2014 to Jan.7th 2015. The U.S. Federal Reserve concluded the last monetary policy meeting of 2014 in mid-December, in which officials stayed positive and emphasized the limited economic impact from Russian crisis on the U.S. and the high possibility of interest hike with the condition of 2% inflation. The recently reported inflation for November 1.3% showed a big gap from the target value. Compared to the U.S., EU is deeply influenced by Russia in terms of economy. Ruble tumbled 41% due to the sanction of the U.S. and EU over the Ukraine issue and the intensifying competition of crude price. The sharply-rising inflation aggravates the Russian economy and harms euro zone accordingly. Besides, Greece’s parliamentary election at the end of January will rise the question about the nation’s membership in the single currency block, which is a key point to watch in the short term.

China’s annual Central Economic Work Conference is another key point to watch to determine China’s economic policy in 2015. The officials in the conference revealed to adapt to the slowing growth, which is viewed as “new normal”. With the goal of “steady growth”, the monetary policy in 2015 is expected to be accommodative. China’s GDP growth target is cut to 7%, according experts, despite the number was not mention in the conference. Japan’s Cabinet reported a revised value of GDP growth -1.9% for Q3, lower than projection. Even so, people continued to vote for the ruling party led by Abe in the parliamentary election, as there is no better option, in hope that Abenomics will bring long-term benefits. BOJ holds the stance on the loose monetary policy and indicates the possibility of more tools. Overall, the U.S. economic outlook is positive compared to other major economies, while Europe and Japan struggle. China’s economy will stay relatively steady as long as no risks emerge.

In 2015, panel prices tends to be conservative. Based on WitsView’s panel price report, the price increase of 55”-and-under panels ended. With the utilization lowered by the annual maintenance and the advanced procurement by downstream makers due to fewer working days during Lunar New Year holidays in February, the TV panel prices in January stay flat, expected to continue through February. IT panel prices drop further after declining in December. In the traditional slow season, the monitor panel prices decline as brands’ restocking momentum weakens and the application absorbs the TV and NB panel capacity. NB panel prices see possibility to stumble in January as it is affected by both the weak demand and panel makers’ inventory clearance. The market buzz CES held in Las Vegas indicates a few signs about the trend in 2015. While 4K TVs are revealed by all brands, curved TVs stay niche items on which brands put all efforts to develop. WitsView expects the penetration rate of curve TV to rise from 0.5% last year to 2.5% in 2015. Chinese brands perform strong ambition in the show, and with extended booth, product lineup, and advertisement, Chinese companies will be more aggressive to compete for the market share with Japanese and Korean brands. In the 1st quarter of 2015, despite of the declining IT panel prices, prices of TV panels, accounting for 75% of the total demand area, stay firm, and prices continue to withstand the slow season.

More detailed analysis is provided to WitsView Intelligence members. Interested in being Intelligence members? Contact us! mkt@witsview.com