MCI Rebounds, Panel Makers’ Excellent Performance in Q3 Shows Possibility of Steady Growth in Next Quarter

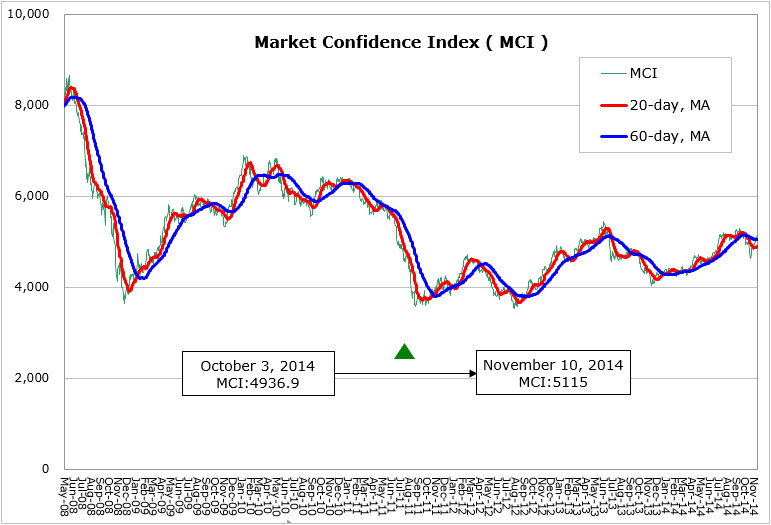

According to Witsview’s latest data, MCI jumped 178.1 points from 4936.9 points to 5115 points from October 3rd to November 10th. In October, Fed’s FOMC has decided to end the third round of quantitative easing. To maintain the long-term growth momentum, Fed announces to keep the short-term interest rate near zero for a considerable time. In addition, the U.S. GDP growth reached 3.5% in Q3, stronger than expected, and the unemployment rate dropped to a current level of 5.8% from 8.1% in 2012. However, the world’s No.1 economy has to deal with the inflation rate lower than the 2% target, which is closely related to the interest hike. In euro zone, Germany performed unideal economic result, and the economic growth forecast for 2014 and 2015 is revised down to 1.2% and 1.3%. The austerity measures will be forced to be adjusted, and the public spending worth 10 billion euro will be injected to the market before 2018 to stimulate economy. ECB’s interest meeting on November 6th held benchmark interest rate unchanged and indicated the risks remaining in the euro zone, therefore the asset purchase program will continue through mid-2016.

From mid-October to early November, China’s Development and Reform Commission has approved the RMB 700-billion infrastructure construction plan, suggesting the Chinese economy needs policy stimulus. The National Statistics Bureau reported GDP growth of 7.3% for Q3, a new low for the five and half years, and the necessity to add infrastructure investment by the government is highlighted. Bank of Japan announced to further ease monetary policies on October 31st, and the yen sharply depreciates to 115 per dollar, a new low for seven years. The Bank of Japan will do "whatever it can" to hit its 2% inflation goal, Governor Haruhiko Kuroda said. Despite of the rising CPI in Japan, the domestic economy shows no expansion, which is reflected to the continuously-growing trade deficit and mounting corporate costs. As the economy in Europe and the U.S. stays steady, China and Japan reveal diverse stimulus measures to stir economy, especially Japan’s monetary easing that would further affect the monetary policies in main nations.

With the panel makers’ quarterly results being reported, the financial results of Taiwan-based AUO and INX and Korean maker LGD all showed steady profits. Samsung electronics’ panel division saw operating revenue remaining positive despite of the declining trend. It showed the strong demand in the market in Q3, which helps digest capacity, lift panel prices, and support ideal profit gains. As we are in the middle of Q4, based on Witsview’s panel price report for the 1st half of November, some sizes of TV panels see rising or flat prices. It shows the market holds an optimistic attitude toward the LCD TV demand in Q4, which is also supported by the steady economy in the U.S. and Europe and the replacement demand in emerging markets. Besides, as the TV market’s demand for larger-sized and high-resolution products surges, the capacity is also digested. The monitor panels show flat prices as makers start to adjust inventory. The NB prices in Q4 dropped as the NB panel demand weakened, along with the elevated inventory and upcoming slow season, after brands’ excellent shipment performance in Q3. WitsView forecasts the monthly shipment growth will only drop slightly 1% in October, which will support the overall panel demand. Despite panel makers would retain profits in Q4, the market share competition will escalate in H2’15 as Chinese and Korean makers’ capacity gets operational and Taiwanese makers announces the capital expansion next year.

More detailed analysis is provided to WitsView Intelligence members. Interested in being Intelligence members? Contact us! mkt@witsview.com