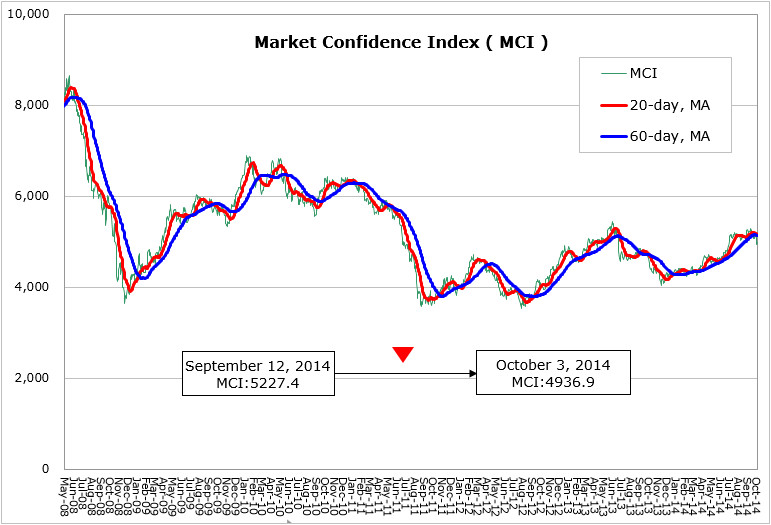

According to Witsview’s latest data, MCI declined 290.5 points from 5227.4 points to 4936.9 points from September 12th to October 3rd. Although the U.S. economic reading showed signs of easing, the two major announcements in the month suggest the world’s largest economy remains on the path of mild recovery. Firstly, the Fed’s meeting minute showed officials came to the consensus to reduce the bond purchase from $150 billion per month to 100 billion and to withdraw the QE in October. In addition, its latest economic outlook report revises up the interest rate forecast for the next two years. All the figures imply the confidence in the U.S. economic outlook. Secondly, the Department of Commerce releases the Q2 economic growth, 4.6%, the highest since Q4 2011, and the economic growth is expected to sustain in H2’14. Meanwhile, the European economy is struggling and ECB applies all possible tools, including interest cuts and LTRO to revive the economy, which however contributed to limited growth. The last measure “Full QE”, the purchase of European government bonds, failed to be carried out due to the lack of consensus among central bank officials. In particular, Germany opposes the stimulus measure and supports to continue the austerity measures despite of the recent risks of economic recession.

China announces fine-tuning measures to boost economic growth. In September, PBOC implements SLF (Standard Lending Facility) by pumping 100 billion yuan to each of the top 5 banks for a three-month period. Besides, PBOC officials lower the interest rate on the 14-day repurchase agreements, a short-term loan to commercial lenders, from 3.7% to 3.50% to reduce the cost of fund. Short-term operations are applied to increase market liquidity and boost economic momentum. More aggressive monetary easing measures are expected later as long as the Chinese economic growth stays soft. Meantime, Japan is suffering from the lack of economic momentum while the Cabinet revises down the economic forecast in its report issued in September. The final PMI manufacturing reading for September dropped from 52.2 to 51.7, raising the possibility BOJ would further loosen the monetary, leading to a sharp drop in yen, coming to 110 yen/ USD, the lowest level since 2008. However, if the Japanese economy will be revived remains unknown. Major economies, except for the U.S., suffer from worsening news and bring negative impacts to the demand side, and the sales should be watched closely.

China’s National Holiday sales kicks off the worldwide holiday sales season. TV brands are fully ready for the promotions. According to Witsview’s survey on retail prices in September, the selling prices of mid-to large-sized LCD TV declined 3%-8% from the previous month, with some sizes even seeing more-than-10% decline. In particular, most sizes of 4K2K 3D TVs and curved TVs showed price drops, which is related to brands’ promotions in China. As the TV sales end, brands would inevitably adjust the inventory and panel purchase according to the year-end financial report. The NB application saw its demand begin to decrease in October despite of the positive factors, including bidding projects for commercial models and OS subsidy offered by Microsoft in Q3. The Q4 NB purchase momentum may be weaken and the panel procurement will cool down as European vendors restock NB in advance while expecting depreciation in euro and the softening Chinese economy damps the demand. Based on WitsView’s survey on panel prices, IT panels and mid-to large-sized TV panels show mostly flat prices without increases, indicating prices are no longer supported by the optimism in the market but driven by the actual sales.

LGD announces to officially have it G8.5 in Guangzhou operate in early September, indicating Korean panel makers are getting aggressive to share the panel capacity market with the favorable terms offered by the Chinese government. China puts every effort to support the local panel makers, and several G8.5 fabs are projected to MP in the next two years. With the significantly increasing capacity, panel makers will have a rarely-seen prosperous year in 2014 with the growing TV sizes and rising 4K TV penetration rate, from 1% last year to 6% this year.

More detailed analysis is provided to WitsView Intelligence members. Interested in being Intelligence members? Contact us! mkt@witsview.com