With Upcoming Investor Conferences, Panel Demand and Supply to be Observed through Q4

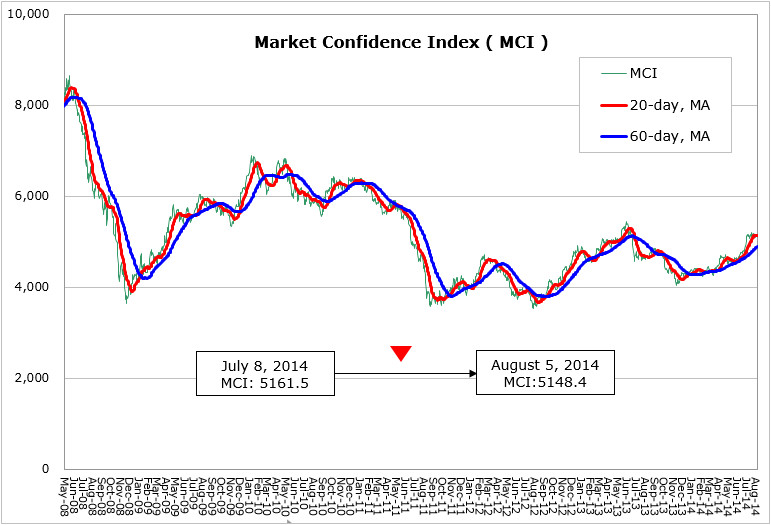

Based on the latest data, the MCI fell 13.1 points from 5161.5 points to 5148.4 points from July 8th to August 5th. The U.S. Federal Reserve’s meeting minutes revealed in July indicates the timing for the withdrawal of QE in October with the condition that the economic recovery meets the expectation, and the policy would end with the last debt purchase amounting to USD 15 billion.

The tension rises in the Eurozone after the Malaysia Airline plane crash, and as the U.S. and Europe escalate sanctions to Russia, the impacts resulted from imported energy and material would drag down pace of the rebounding economy in the single currency area. The ZEW index shows the July reading dropped largely from 58.4 in the previous month to 48.1, weaker than projected.

The sixth joint-meeting of the U.S.-China Strategic and Economic Dialogue held in early July reached the consensus to reform the Chinese exchange market. The previous RMB appreciation didn’t fully correspond to the actual economic changes, and the Chinese currency remains undervalued. People's Bank of China Governor Zhou Xiaochuan indicates the intervention on RMB exchange rate would be trimmed and the exchange rate flexibility would be improved only under certain conditions. It shows downward economic pressure would inevitably surpass the bilateral consensus. The HSBC’s latest China PMI reached an 18-month high, rising 1.3 points to 52, showing the micro stimulus get influential. The policy stimulus and deregulation are currently key economic guidelines in China.

As we enter Q3, a series of investor conferences start. The leading panel maker LG display sees the net profit rising 143.3% YoY, significantly improving from Q1. The electronics giant Samsung’s financial forecast in Q2 showed risks of dropping operation revenue and profits, while Apple’s sales stays shy of projection, indicating the keen competition among makers.

According to WitsView’s panel shipment report, the LCD TV panel shipment in June rose 0.6% MoM, implying the continuously heating up LCD TV panel demand. However, the Black Friday sales in Q4 would be the turning point for makers to digest panel inventory. As the TV panel demand is impacted without surprise, the panel capacity transfer to LCD monitor panels would also affect the balance and influence prices. Besides, the new-generation large-sized iPhone would squeeze the room of survival for other mobile devices, especially the Android smart phones and tablets, and bring uncertainties to the mobile device panel demand in 2H’14.

More detailed analysis is provided to WitsView Intelligence members. Interested in being Intelligence members? Contact us! mkt@witsview.com