Market Confidence Continues to Climb, Q2 and Q3 Outlook Stays Relatively Positive

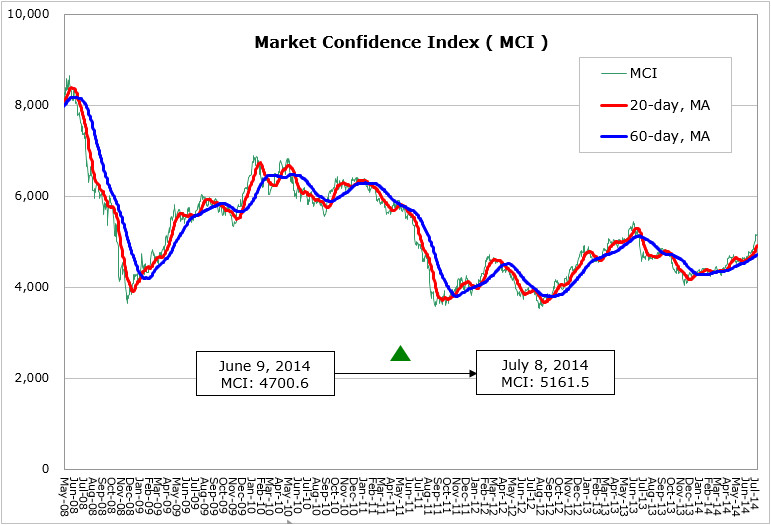

Based on WitsView’s latest data, MCI rose 460.9 points from 4700.6 points to 5161.5 points in the period from June 9th to July 8th. In mid-June, the Federal Open Market Committee under the Federal Reserve has cut the debt purchase amount for the 5th time amid the positive economic outlook after the monetary policy meeting, meanwhile the federal fund rate is expected to rise at the end of 2015 and even in 2016. However, the market remains both optimistic and cautious and the federal fund rate would stay low, around 0-0.25%, in 2014, while the long-term interest rate projection is lowered from 4% to 3.75% in response to the slowing economic growth in U.S. The final reading of composite PMI for the euro zone in June trimmed from 53.5 in the previous month to 52.8. As the downward economic pressure intensifies for the single-currency zone, ECB is forced to implement the second measure “Long-Term Refinancing Operation”, which was repeatedly employed previously and is projected to be applied six times from 2015 to 2016, following the negative interest rate policy announced earlier.

China’s indicative index rebounded in June, the manufacturing PMI by HSBC attained the new high in six months, climbing to 50.7, while the service PMI rose to 53.1, the 15-month high, which is strongly supported by the “micro-stimulant” policies. Amid the downward economic risks in Q1, the Chinese government has implemented 17 similar measures to stabilize the growth since mid-April. The Japanese economy has recently focused on “the third arrow” as Prime Minister Shinzo Abe on June 24th announced several stimulant policies including to encourage female labor participation and increase immigrants to revive the shrinking workforce market, boost enterprise investment, and reduce corporate tax. Despite the result remains to be observed, the officials’ ambition to propel growth cannot be underestimated.

As we enter Q3, the panel demand is continuously supported with the help of back-to-school sales and promotion for Black Friday. In addition, Chinese top six brands share the overseas market due to the weak domestic demand and lift the export proportion, while Panasonic and Samsung’s withdrawal from the PDP market drives up the LCD TV shipment. According to the large-sized panel shipment report by WitsView, the LCD TV, monitor, NB, and tablet panel shipments in May climbed 1.5%, 2.9%, 9.3%, and 12.3%, respectively. WitsView’s panel price report for the first half of July shows the large-sized 65” panel price declines $5, a few sizes see small price increase, while the remaining sizes see no price changes. The factor resulting in rising demand and flat prices is buyers are constantly pressured by the price increases and take a conservative position on demands in an attempt to lower prices, which leads to a wait-and-see attitude for both demand and supply sides and slight price increases.

As China and Korea are expected to complete the negotiations on FTA at the end of the year, the range of tax exemption on panels is closely watched by panel makers. While China and Taiwan are deeply related in terms of panel demand and supply, the possibly conditional tax-exemption on certain sizes of Korea-produced panels would affect the production and shipment competition among makers, which would even contribute to future growth and decline in panel makers’ influences.

More detailed analysis is provided to WitsView Intelligence members. Interested in being Intelligence members? Contact us! mkt@witsview.com