Delayed Spring Swallow: Multiple Factors Lift Demands, Panel Makers’ Business Pressure Eases

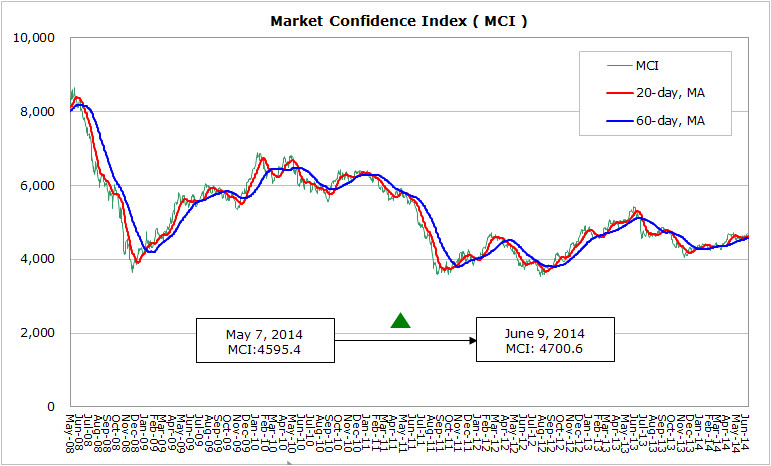

According to WitsView’s latest data, MCI rose 105.2 points from 4595.4 points to 4700.6 points from May 7th to June 9th. The U.S. economy would see a rebound in Q2 after a temporary stagnation in Q1, and the final composite PMI reading for May grew to 58.4 from 55.6. The June-4th edition of Beige Book, having eight issues per year by the Fed, reveals an assessment of the current economic condition, which indicates a mild economic growth on the path of sustainable recovery. The economy in the euro zone has been showing slow recovery, which is viewed as insufficient. The data by Eurostat indicates the Q1 GDP growth in the single currency zone rose 0.2% QoQ and 0.9% YoY. In addition, the inflation rate in May was only 0.5%, far from EBC’s target 2%, which forced the central bank to announce to cut the interest rate and even introduce a negative deposit rate on June 5th. If the unprecedented and bold act would propel sustainable effect remains to be seen.

Recently, international institutions simultaneously revise down the forecast for China’s economic growth. IMF, following OECD, cuts the projection of Chinese economic growth from 7.3% to 7%. In view of this, the Chinese officials hold a cautious attitude, and in the consecutive eight executive meetings of State Council, officials have proposed the implantation of “micro-stimulation economic policy” to reach the goal to stabilize growth. On one hand, it prevents from the rapid growth decline, and on the other hand, how to handle shadow banking and the credit risks including municipal debts needs to take into account. How to keep the fragile balance between the two is a severe challenge for the world’s second largest economy.

As Q2 comes to the end and in a time between spring and summer, panel makers finally greet the market rebound. WitsView’s latest large-sized panel shipment report indicates 5% MoM shipment growth and panel makers’ aggressive shipment rush in May as it is supported by optimistic atmosphere at the demand side, including the PDP TV withdrawal from the market that stirs the LCD TV sales, Mexico’s plan to announce subsidy policy on small-sized LCD TVs, the economic recovery in western nations which boosts the TV demand, and the TV replacement sales in emerging markets helped by the FIFA World Cup Games.

With the rising demand, constantly climbing panel prices temporarily ease panel makers’ pressure on profits. According to the panel price survey for the 1st half of June by WitsView, only a few large-sized TV panels see price drops, while most LCD monitor and NB panel prices stay on par with some sizes even seeing price increases. However, if Taiwanese makers constantly generate profits and Korean makers swing from losses to profits after Q2 or Q3 relies on the fundamental issues such as appropriate capacity control and healthy inventory level. Besides, with the G8.5 capacity continuing to start operation in China, Q3 would be the turning point for prices to collapse or stay supported.

More detailed analysis is provided to WitsView Intelligence members. Interested in being Intelligence members? Contact us! mkt@witsview.com