Market Confidence Steady, Optimistic Outlook for Q2, Panel Makers Likely to Improve Business

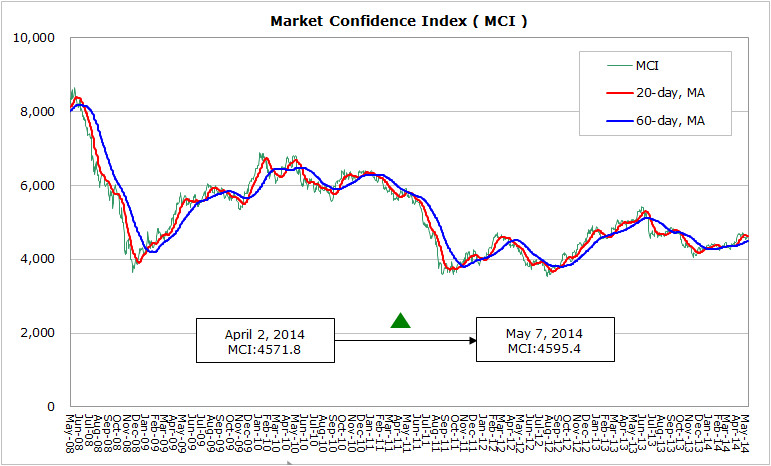

According to WitsView’s latest data, MCI rose 23.6 points from 4571.8 points to 4595.4 points from April 2 to May 7. The index declined in May after a temporary surge in April. In the beginning of May, the U.S. Commerce Department published the economic growth of only 0.1% for Q1, while the U.S. composite PMI’s final reading came to 55.6, higher than the initial estimation 54.9 and comparable to March’s final figure 55.7. The data suggests the economic recovery may be delayed to Q2. Eurozone’s composite PMI for April rebounded to 54, higher than that in March and staying above the threshold 50 for ten consecutive months. The economic recovery in Europe is steady, while officials of EU Commission warn about the potential risks in Ukraine.

Based on the Annual Economic Outlook Report issued by OECD, China’s 2014 economic growth is cut to 7.4%, and both HSBC manufacturing and service PMI declined in April, to 48.1 and 51.4 respectively. Despite the slowing economic growth in China is inevitable, the concerns about the immature financial system and recent housing-bubble burst need to be handled properly. Japan’s Prime Minister Shinzo Abe has encountered obstacles when loosening the regulation of the labor market, and in addition, the issue of relatively low female labor participation rate causes waste of labor forces. If the third arrow of Abenomics can be launched smoothly relies on the Cabinet’s determination.

Major panel makers have published Q1 financial statements, as Korea-based LGD and Samsung showed losses instead of profits. On the other hand, Taiwan-based AUO and Innolux barely retained positive gains due to the differences in product portfolio strategy of Taiwanese and Korean makers. In view of the industrial movement, WitsView’s panel price report for the first half of May shows that the prices of TV, LCD monitor, and NB panels stop dropping and prices of certain sizes continue to rebound. Looking ahead to Q2, May 1st holidays in China, FIFA World Cup in June and the PDP TV replacement sales all propel the panel demand. As for monitor and NB panels, Microsoft halting support to XP indirectly boosted the LCD monitor sales in the commercial market, while new NB model launches stimulated the demand for mid-and-small panels. To sum up, the panel demands of all applications stay relatively healthy and are likely to help panel makers’ business in Q2.

More detailed analysis is provided to WitsView Intelligence members. Interested in being Intelligence members? Contact us! mkt@witsview.com