Market Confidence Rebounds Slightly, Tight Panel Demand and Supply in Long-Term Key to Makers’ Profits

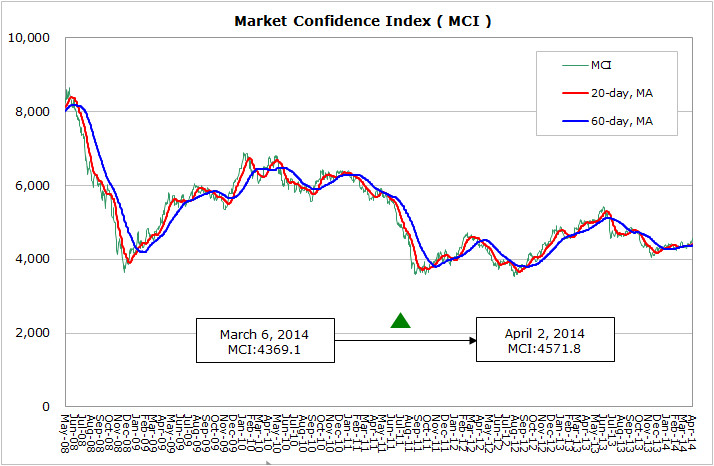

According to WitsView’s latest data, MCI rose 202.7 points from 4369.1 points to 4571.8 points from March 6th to April 2nd. The U.S. Federal Reserve chief Janet Yellen’s talks on QE has brought turbulences to the global financial market. In mid-March, the chairwoman implied the interest rate may rise six months after the end of bond purchase program, which damped the market. However, she indicated on March 31rd to continue the QE “for a while” due to the relatively high unemployment, boosting the market confidence. In view of Chicago PMI for March, it dipped to 55.9, the lowest since August last year, and shows the U.S. economy still needs momentum to sustain. The composite PMI for March in euro zone declined 0.1 to 53.2, and the inflation rate has stayed below 1% for six consecutive months, far from reaching ECB’s target 2%. Besides, the U.S. and Europe have conducted several sanctions to Russia on the Ukrainian issue, showing the unclear outlook for European economy and the fluctuations in energy and grain prices which may be a future concern.

Since the end of February, yuan has showed deep depreciation against USD, from 6.07 on February 19 to 6.2 on April 3. China’s central bank has expanded yuan trading band to 2% from 1% in March 17 after Premier Li Keqing proposed the measure as the National People’s Congress ended. As China loosens exchange rate control, it accelerates the yuan depreciation to prevent the hot money from flowing in, improve export, and boost economy growth. Japan raises sales tax to 8% on April 1st , which is contrary to Abenomics but inevitable as Japan’s public debt comes to 200% of GDP. When facing the new impacts, Abe’s cabinet needs to strike a balance between deficit cuts and economic growth.

As for the movements in the industry, WitsView’s historical panel price data indicates the continuous panel price declines since the 2nd half of last year and the panel demand side turns cautious. In addition, the holiday promotion and the labor shortage in February this year lower the panel inventory. The depreciation in yuan boosts the panel costs and prompts the Chinese panel makers to increase the panel demand on psychological factor. Moreover, brands launch new spring models, followed by the demands for May 1st holidays in China and World Cup Games, and the panel demand is expected to rise. Based on WitsView’s analysis on large-sized panel prices, the 32”, 40”, and 42” panels are tightly supplied due to Korean makers’ strategies. Based on the factors mentioned above, the demand and supply in the panel market get tighter from previous, supporting the market confidence to rebound slightly. However, the end demand is not strong, and if the highly-anticipated and representative sales performance during China’s May 1st holidays is poor and brands and panel makers’ inventory is not adjusted, the demand and supply unbalances will aggravate and lead to panel price declines. Makers’ control of the situation will determine the profits or losses in the 2nd half of the year.

More detailed analysis is provided to WitsView Intelligence members. Interested in being Intelligence members? Contact us! mkt@witsview.com