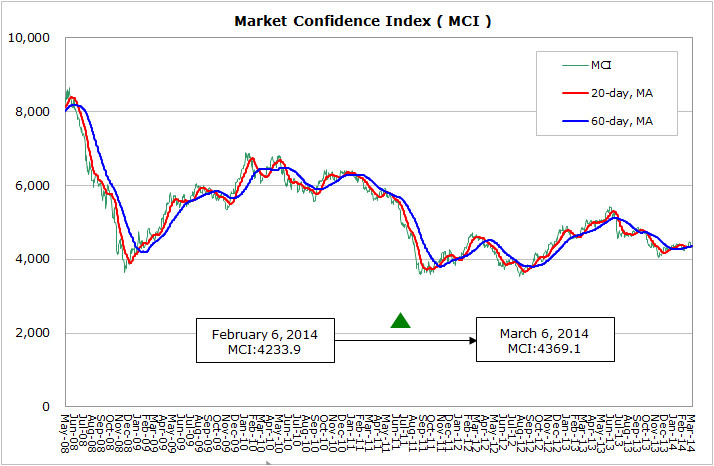

According to WitsView’s latest data, MCI jumped 135.2 points, from 4233.9 points to 4369.1 points, from Feb 6th to Mar 6th. The U.S. composite PMI, combining the manufacturing and services, had a final reading of 54.1 for February, lower than the previous forecast and 56.2 for January, reflecting the short-term impacts of the extreme weather. The U.S. Federal Reserve’s Beige Book released on March 5th indicates the slow and steady recovery in the U.S. economy if the weather factor is not taken into account. The February political turmoil in Ukraine prompts the EU to announce economic sanctions on Russia’s troops entering the eastern-European nation, despite of emerging differences inside the union as its member states are deeply dependent on Russia economically. The February composite PMI reading for the euro zone came to 53.3, higher than the January result, the deflation stayed mild, and the recovery continued. However, the European economy would be dragged down if the crises in Ukraine are not solved effectively.

China’s annual National People’s Congress opens on 5th March, and despite of the slowing economy, Premier Li Keqiang has announced an economic growth 7.5% for 2014, a target for three consecutive years. With the economic situation getting complicated and difficult, officials from National Development and Reform Commission indicate the possibility to intervene and readjust as long as the downward signs emerge. China’s HSBC composite PMI for February came to 49.65, the second lowest on record, and it suggests less optimistic growth for Q1 2014 in the country on top of the Lunar-New-Year-holiday factor.

The panel industry enters the traditional slow season in Q1, and the market confidence stabilizes from the previous month despite of softening demands. Based on WitsView’s historical panel price record, the panel prices drops have been narrowing from January to March. Moreover, WitsView’s latest panel price survey reveals that in H1 March only large-sized TV panel prices are pressured due to the inventory to be digested, while panel prices for tablets, monitors, and NBs are relatively stable. Some sizes even show rising prices as China’s labor shortage is not yet solved. Despite of slowing price drops, panel makers’ utilization has no major cuts, and with the featured products, such as 4K2K TV, stirring no significant demand in the market, the oversupply concern for panels remains in Q2. With the short-term demand staying unclear, if the unbalances between demand and supply will ease depends on panel makers’ execution of utilization adjustment, which is also the key to panel prices and makers’ profits.

More detailed analysis is provided to WitsView Intelligence members. Interested in being Intelligence members? Contact us! mkt@witsview.com