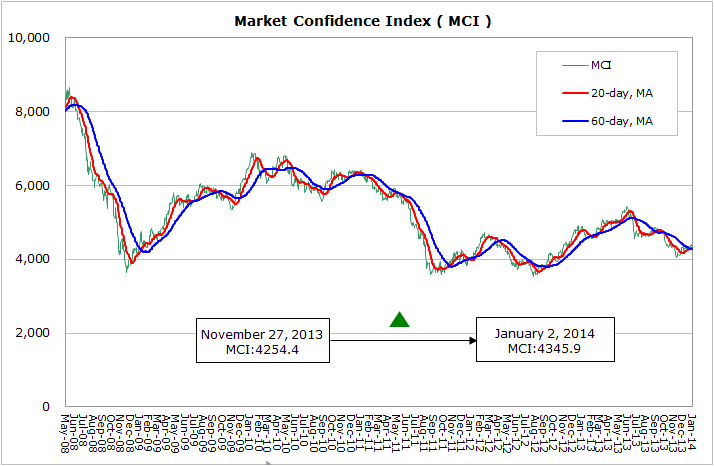

According to WitsView’s latest statistics, the MCI, after dropping deeply from September to November, showed signs of recovering for the first time in the period from November 27, 2013 to January 02, 2014, and it jumped 77.4 points from 4268.5 points to 4345.9 points. As we greet 2014, the dawn is seen in the U.S. and European economies, the U.S. PMI climbed continuously from 57.3 to 59.1 in December, and the U.S. consumer confidence revealed on 31th came to the three-month high 78.1 as it sees the basis period as 100 in 1985. Fed has announced finally in mid-December to wind down the debt purchase program from January 2014, indicating the sustainable economic growth in the U.S. Euro zone as a whole shows recovery as ECB indicates no need to further cut interest rate for the moment, however, imbalances remain in different member states. The December PMI in euro zone surged to 52.7 from November with indicators for Germany and France showing distinct results as the manufacturing PMI in the former reached the 30-momth high, 54.2, while that in the latter dipped to the lowest for seven months.

China’s official PMI for December was published on January 1st, which was the lowest for the 4 months, 51.0. The HSBC’s PMI came to the three-month low, 50.5, suggesting large national corporates and medium-and-small private enterprises were seeing slowing growth. Besides, China’s National Audit Office revealed a total amount of RMB 17.9 trillion of municipal debt, adding RMB 7.2 trillion from 2013, as local governments’ expenditure accelerates both strong economic growth and debt default risks, and it depends on Chinese officials’ action to ease the impact to drag down the economy. Japan’s recent political moves may stimulate economic turmoil with its neighbor nations in Asia, and as it raises consumption tax in April 2014, the showing quarterly economic growth and the possibly ending deflation need to be observed.

The bright spot in the TFT-LCD industry is the continuously expanding capacity with Samsung’s Gen 8.5 in Suzhou ready in October 2013, BOE’s Gen 8.5 in Hefei getting operational at the end of December, LGD’s Gen8.5 in Guangzhou starting operation in June 2014 and AUO’s Gen8.5 in Kunshan starting mass-production. Moreover, in 2015, CEC-Panda’s Nanjing Gen8.5 plant, CSOT’s Gen8.5 of the 2nd phase, and BOE’s third Gen 8.5 in Chongqing will start productions. WitsView believes in the new year 2014, Chinese panel makers are getting obviously aggressive with government’s capital support and tariff barrier that encourage the national makers to dominate the industry. The competition among panel makers will intensify in 2014 with profits being further pressed down, and makers have to seek the long-term sustainable niche market on top of the low-price strategies.

More detailed analysis is provided to WitsView Intelligence members. Interested in being Intelligence members? Contact us! mkt@witsview.com