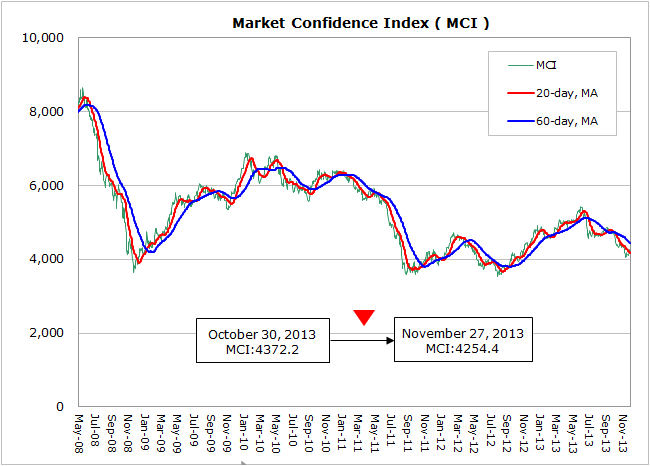

Base on WitsView’s latest survey, MCI dropped 117.8 points from Oct 30th to Nov 27th from 4372.2 points to 4254.4 points. As we observe developments in major economies, the U.S. PMI for manufacturing and service industries jumped respectively from 50.6 and 49.3 to 54.3 and 57.1 in October, indicating industries in the U.S. are leaving the impacts of government shutdown behind, however, according to the quarterly survey published by Philadelphia FED on Nov. 25, economists are not optimistic about the outlook in Q4 and Q1 next year, the Q4 growth forecast is cut from 2.5% to 1.8% and the Q1 projection is down from 2.7% to 2.5%, indicating sluggish economic performance in the world’s largest economy. The composite PMI in the euro zone for November is down from the final reading of the previous month 51.9 to 51.5, the lowest for three months, in addition, ECB unexpectedly cut the interest rate early this month, and even September’s largest trade surplus in ten years cannot ease the concern of the insufficient growth momentum in the single-currency area.

The initial reading for HSBC’s China PMI comes to 50.4, lower than 50.9 in October and showing declines for the first time in four months. Despite slightly shrinking economic momentum, Premier Li Keqiang confirms to achieve the economic growth goal of 7.5% for this year. Moreover, the economic overhaul after the third plenary session of Communist Party is set to reduce the government intervention and support the market mechanism in order to keep substantial economic growth as the short-term struggles are inevitable. Japan shows no improvement in trade deficit after the longest-ever trade deficit record set last month, meanwhile, Governor of BOJ indicates to continue the quantitative monetary policy, leading to the recent depreciation in yen. However, the policy brings alarms to Japan’s finance, and how to balance the healthy finance and the depreciation is a test to Japanese officials.

As we are at the middle of Q4, the entire panel industry is struggling. Based on WitsView’s survey on Chinese top six TV brands’ shipments, the Q4 shipment reaches 14.6 million units, rising 2-3% QoQ but dipping 8.2% YoY, and makers have to rely on the demand for 2014 Lunar New Year as China’s domestic demand is weak. As the inventory issue aggravates, some panel makers have to revise down the capacity, but with Chinese and Korean panel makers’ new capacities getting operational in China, the oversupply remains and panel price outlook is not positive. According Witsview’s forecast for TV panel modules and open cells, all sizes show price drops USD 1-9 in November. Witsview believes that the period from the end of Q4 to early next year is crucial, and panel makers’ consensus to cut production will be the key to the following price trend as the pressure of the growing Gen8.5 capacity in China emerges.

More detailed analysis is provided to WitsView Intelligence members. Interested in being Intelligence members? Contact us! mkt@witsview.com