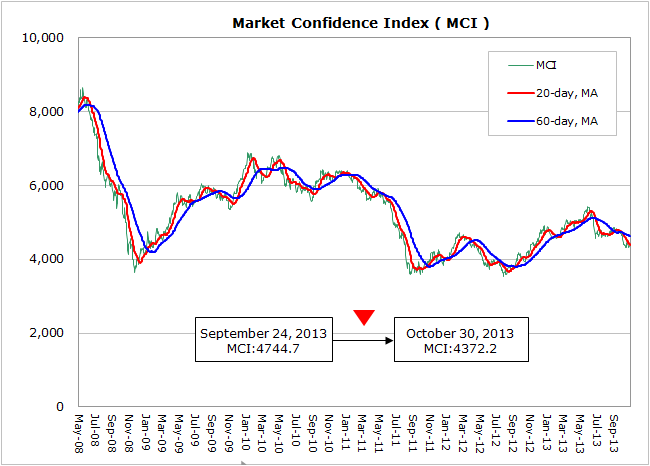

According to WitsView’s latest data, MCI dropped 403.4 points from 4744.7 points to 4341.3 points from September 25th to October 29th. The weak market confidence suggests the sluggish outlook in the panel industry. After the U.S. bipartisan failure to reach an agreement on the federal budget followed by a temporarily government shutdown for half the month in early October, the gradually market sentiment is again struck. While the October consumer confidence for the U.S. released by Michigan University comes to the ten-month low, the PMI drops to 51.1 from 52.8 in September, lower than the market’s expectation. As the government shutdown ripple effect spreads, the U.S. economy may suffer more harm in Q4. On the other hand, Europe sees smooth recovery, despite the composite PMI declines to 51.5, it remains above the expansion benchmark of 50. However, it is too early to determine the insufficient growth in the single-currency area based on the one-month data while both Germany and France’s growth eases.

China’s PMI continues to climb in October with an initial reading at 50.9, higher by 0.7 than last month’s final data and reaching the seven-month high. In addition to the structure adjustment, the nation’s new overhaul policies are taking effect, reflected on the Shanghai free-trade zone launch. It took only six months from March when Premier Li Keqiang made visits to show his supports to late September, the opening of the zone, demonstrating Chinese officials’ ambition to lift business competitiveness and strengthen the economic system. Japan’s trade statistics indicates the 15th consecutive month of trade deficit in September, setting the longest trade-deficit record on history. It shows both the weaker-than-expected influence of yen depreciation and Japanese economy seeing difficulties to grow with the weak oversea demand.

In view of the industry demand, the sales during China’s Mid-Autumn and National Holidays softened, coming to 491.2 million units and trimming 2.9% YoY, according to WitsView’s latest sales survey. Despite of the lowering inventory of 5.7 weeks for TV brands, it remained relatively high, indicating brands’ efforts to drive up shipments during the holidays were in vain. The panel glut is not a short-term issue, but Taiwanese and Korean panel makers’ utilization stays elevated, around 90%, as we enter Q4 mainly because of makers’ profit concern and attempt to reach sales. WitsView has repeated that the oversupply can only aggravate next year as three new G8.5 fabs are added in China, of which SDC’s Suzhou plant has started to operate at the end of this month, declaring an early bloody price war. If panel makers’ oversupply leads to long-term loss depends on panel makers’ wisdom, who should avoid the neglects resulting in imaginable consequences.

More detailed analysis is provided to WitsView Intelligence members. Interested in being Intelligence members? Contact us! mkt@witsview.com