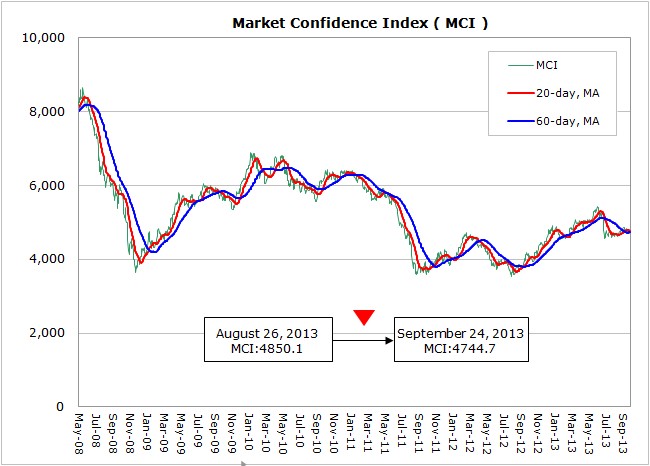

According to WitsView’s latest data, MCI dropped 105.4 points from 4850.1 points to 4744.7 points during the period from August 26th to September 24th. While MCI showed fluctuations, the major events in leading economies were strong enough to shake the market confidence. Firstly, Federal Reserve chairman Ben Bernanke on September 18th announced to postpone the withdrawal of the quantitative easing policy, injecting support to the market, especially the emerging economies. However, the possibility for the policy exit before the end of the year is high and uncertainties remain. The U.S. PMI’s preliminary reading dipped to 52.8 in September from the previous month, responding to the decision of delaying the end of QE. As for Europe, Angela Merkel has won her third term as German chancellor in the parliamentary election, realizing a more stable single-currency union. The euro zone PMI, indicating Germany’s handling of the debt crisis, rose to 52.1 in September, which has stayed above the hurdle between growth and contraction for three months and reached a two-year new high.

China’s implantation of all tuning policies was viewed positive to its economy, and its September PMI continued to climb to 51.2, a six-month high. On the other hand, the PMI surge implied the stabilizing economy could further help the policy overhaul. Japan’s winning of the race to host Olympic Games is viewed as Abe’s “fourth arrow” as the Games would bring tremendous economic benefits to the host country based on the historical experiences. Japan’s current obstacle is the record high debt, and to solve the issue, the officials propose both sales-tax hike and corporate-tax cut to ease the impact. However, it remains a question mark if it tackles the government debts.

In view of the industry, WitsView’s updated panel price survey for the 2nd half of September indicates extending price drops, with USD 5-8 declines for large-sized TV panels. Besides, WitsView foresees trimming LCD TV demands in major markets as Japan has a 26-28% drop, Western Europe shows a 15-17% decline, North America has a 1-3% trim, and only China holds 8-10% growth. Therefore, the Oct 1st holidays in China would be the only competing battle field in Q4 with panel makers emphasizing on 4K2K products as it remains a consumption-stimulating segment and Chinese brands have surging demands for 4K TVs. Based on WitsWiew’s shipment data, the 4K2K TV panel shipment jumped 47% in August from the previous month.

Nevertheless, the intensively talked UD TV has a low penetration rate globally in 2013, unable to lift the sluggish market. With the inventory issue and the pressure of high utilization, the Q4 panel prices may continue to drop and erode panel makers’ profitability in H2’13. On the other hand, as the market expects China to raise the import tariff on panels, Taiwanese makers’ competitiveness advantages may fade in the future. Except for the throat-cutting war, how to hold or even create technology strength is the key to long-term development and to maintain profits.

More detailed analysis is provided to WitsView Intelligence members. Interested in being Intelligence members? Contact us! mkt@witsview.com