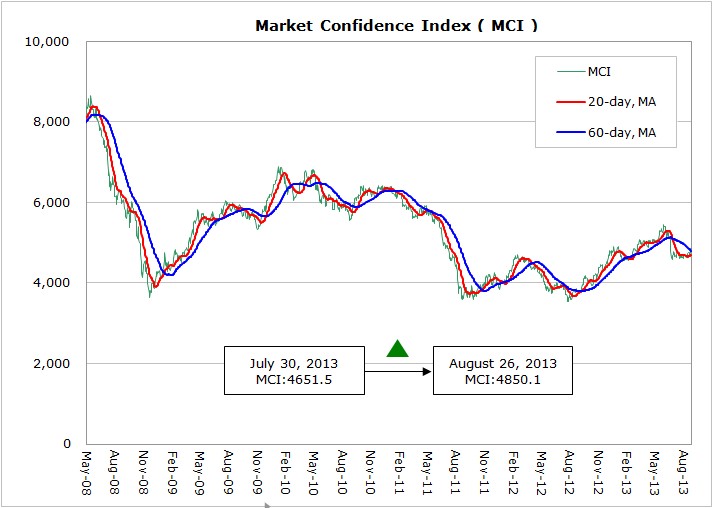

According to WitsView’s latest data, MCI jumped 198.6 points from 4651.5 points to 4850.1 points from July 30th to August 26th. After the fluctuations in the previous period, MCI in August showed a small increase. Europe and the U.S. continue to see stable economic recovery with the U.S. preliminary PMI for August reaching 53.9, growing 0.2 from July. The U.S. Commerce Department has released the Q2 GDP, which surged 1.7% annually and was stronger than 1.1% in Q1. Although the exit of quantitative easing policy is certain, Fed’s exact timing for the measure depends on the U.S. economic improvement progress.

The euro zone’s August PMI followed the expanding trend in the previous month, rising to 51.3, while GDP showed signs of growth and surged 0.3%, leaving behind the contraction for the previous six consecutive quarters. Among these, the European locomotive, Germany, played a crucial role and had a 0.7% quarterly economic growth, benefitted from the warming up export and domestic demands. From an overall perspective, Europe and the U.S. maintain the growth momentum and support a highly anticipated Q3 outlook.

After dropping for the two previous quarters, China’s August PMI rebounded to 50.1 and paused temporarily above the benchmark to expansion. Pressured by the easing growth in the first half of the year, the growth guidance for the second half has been set to the” growth stabilization, the structure tuning, and the reform improvement”. The State Council of China has announced several major policies in July and August, including the remove of interest rate limit, the temporary tax exemption for small enterprise, and the urbane-area infrastructure, which correspond to Li Keqiang’s “mini stimulus” policy. A series of active actions indicate China’s determination to boost the economy, but the basic structural transformation takes fundamental measures in the long term. Japan saw a 0.6% quarterly GDP growth, unexpectedly lower than the market’s projection 0.9%. BOJ Governor indicates more monetary stimulus will be needed if the economy shows risks of declines, suggesting the uncertainties and the insufficient strength in Japan’s recovery.

According to WitsView’s panel shipment data, the global panel shipment dropped 2.8% MoM in July, and the August shipment is projected to show no growth from July. With declining demands, panel makers’ fixed capacities, and the previous inventory to digest, the panel market shows a serious glut. Based on WitsView’s recently released quotation for the 2nd half of August, TV panel prices drop averagely USD 5, and prices for monitor and NB panels continue to decline. Despite of Q3 and Q4 supported by China’s Oct 1st holidays and the year-end peak season in Europe and the U.S., panel prices won’t be largely lifted. One of the reasons is that China and Korean makers’ new fabs in China will soon be operational, expanding the global capacity. Another reason is that to digest inventories, panel makers can only take more aggressive pricing measure to win clients’ orders. Panel makers have to struggle a long way through the end of this year.

More detailed analysis is provided to WitsView Intelligence members. Interested in being Intelligence members? Contact us! mkt@witsview.com