Market Noises and Elevating Price-cutting Pressure Intensify Panel Makers’ Wrestling

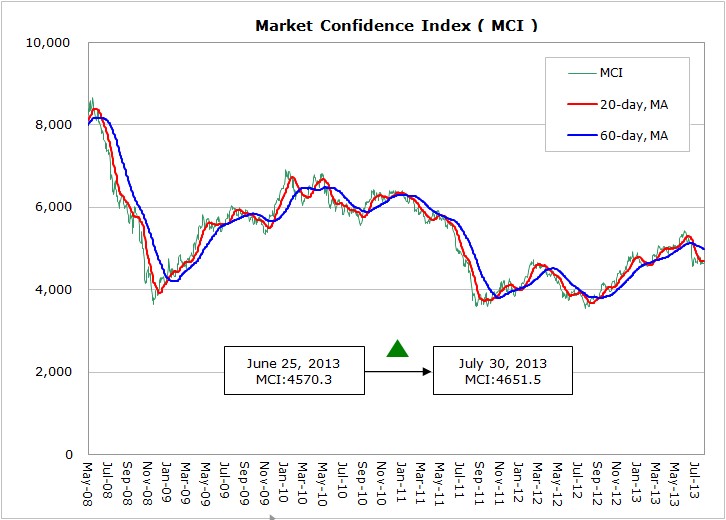

According to WitsView’s latest data, MCI surged 81.2points from 4570.3 points to 4651.5 points from June 25th to July 30th. The index entered a period of fluctuations after a deep drop in June, and the variation was wider than previous, indicating the market full of noises and the inconsistent views on the outlook. However, in terms of the global economy, the U.S. preliminary estimate for the July PMI bounced back to 53.2, reaching the new high for the last four months. But the indicator has seen a declining trend since the beginning of this year, while IMF’s forecast for U.S. 2013 annual growth is only 1.7%, showing a tepid recovery for the world’s largest economy. The preliminary PMI in the euro zone in July topped 50, rising to 50.4, for the first time for the last 18 months. If Q3 can revive from the recession depends on the growth trend.

China is facing a completely different situation, seeing an economic growth softening for two consecutive quarters and a July PMI dropping to 47.7, under the benchmark dividing the expansion and the contraction and lowest level since the 2009 financial crisis. It reflects not only the risk of the weakening economy but issues on economic adjustments and restructures. Japanese Prime Minister Abe’s government follows the U.S. and takes the quantitative easing measures to attract oversea capital and stir domestic investments, which is eventually seen as an act to encourage hot money inflows instead of benefitting medium and small businesses and consumers, and the long-term impacts are being evaluated.

For the panel industry, according WitsView’s data, the global large-sized panel shipment declined 7.7% in June as makers were obligated to maintain sales performance under the semi-annual financial statement pressure and the Chinese panel makers were supported by the government and expanded the Gen8.5 capacity to lift shipments and share the market. WitsView indicates as July is the traditional slow season, the shipment will drop 10-11% from June. But the panel price drops may widen in July due to the weakening global economy and the declining demands in China after the slight decreases in the previous month, showing an inevitable demand-and-supply imbalance. Meanwhile, how panel makers react is the point to observe in Q3.

More detailed analysis is provided to WitsView Intelligence members. Interested in being Intelligence members? Contact us! mkt@witsview.com