Demand-supply Imbalance Causes Drop in Panel Prices, Market Confidence to Rise?

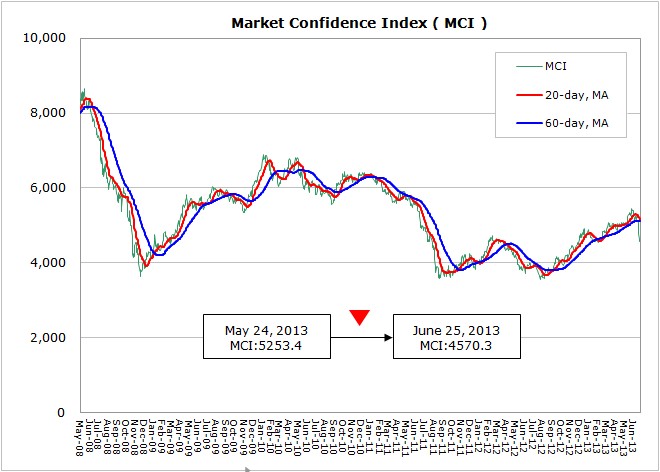

According to WitsView’s latest data, MCI dropped 683.1 points to 4570.3 points from 5253.4 points from May 24th to June 25th. MCI has declined deeply since June, showing the insufficient market confidence and the outlook uncertainties. The most shocking news to the global economy is the speech by Ben S. Bernanke, Federal Reserve Chairman, who clearly indicates when and how the quantitative easing policy will end. Despite the market will be back to fundamentals, the fluctuations are inevitable, and if the market confidence can be established firmly depends on the industry growth strength. For PMI, the reading for the U.S. dipped from the May final result 52.3 to 52.2, the primary reading in June, showing the softening manufacturing in the world’s largest economy. The initial PMI in the euro zone reaches 48.9 in June, higher than 47.7 in May but still lower than the threshold 50, and it is a long way for the economy to stand firmly and leave the contraction behind.

After releasing the weakening macro economy indicators in May, China’s “Keqiang’s index”, consist of industrial electricity consumption, railway transportation volume, and mid and long-term loan, drops to the record low. Additionally, HSBC’s China PMI in June decreased to 48.3, weaker than the May final reading 49.2 and below 50 that divides expansion and contraction, reflecting the declining trend in the Chinese economy. Besides, China’s central bank, PBOC, made a warning speech on 24th this month regarding to the credit squeeze that has lasted for a month, stating the stand not to clean the mass for banks.

The market is certain China’s Premier Li Keqiang will lead the new government and carry out his “steel and blood” policy to the financial industry, constantly weakening market’s confidence to the financial system. Moreover, analysts have revised down the forecast for China’s GDP this year, from conservative to worsening. For Japan, Prime Minister Abe’s “three arrow policies” seem to stumble as the currency policy cannot maintain the drop in yen, the quantitative easing policy shows limited influences to Japanese economy, and the third arrow “industrial structural overhaul”, which has to transform how the Japanese economy functions from the foundation, is difficult to be executed.

In the stagnant environment and in view of the industrial production, despite the waning panel demand, the panel supply is not reduced appropriately according to the market changes, based on WitsView’s utilization survey data on panel makers. Taiwanese makers’ utilization is planned to be relatively high in Q2 and Q3, including the leading maker AUO who holds 88% of utilization in June and foresees a 90-92% level in Q3. Innolux, seeing the similar trend, has 92% of utilization in June and expects a 92% level in Q3. According to WitsView’s panel shipment survey, the large-sized panel shipment in May attained 67.65 million units, surging 4% MoM, and the oversupply trend continues and leads to significant price-cutting pressure. At the middle of Q2, makers should ease the demand-supply imbalance when looking forward to the peak season in H2’13.

More detailed analysis is provided to WitsView Intelligence members. Interested in being Intelligence members? Contact us! mkt@witsview.com