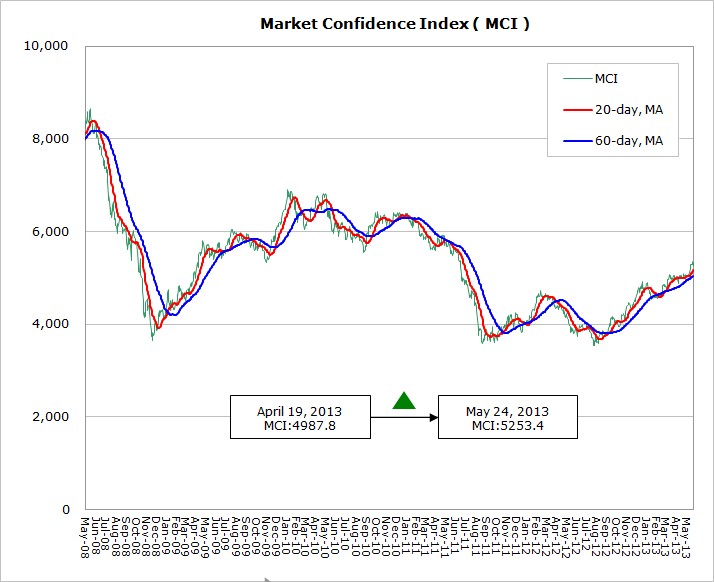

According to WitsView’s latest data, MCI jumped 265.6 points from 4987.8 points to 5253.4 points from April 19 to May 24, with the index swinging between gains and losses in April and seeing realistic surges in May. The macroeconomic indicators in April were tepid as the U.S. PMI dropped to the lowest level, only 50.7, since December last year, the deficit cutting mechanism started to take effect, and the U.S. economy showed signs of stagnation. Meanwhile, the European economy saw no recovery, and the April PMI of was 46.9 for the single currency zone, showing the contraction for the 15th month and a recession risk that cannot be got rid of in Q2.

China’s official PMI dropped to 50.6 which was lower than the market’s expectation, particularly the export orders fell below the benchmark dividing expansion and decline, and the reading suggested the uncertainties in the global demand and the unstable stimulants to China’s economic growth. As for Japan, the good news came with the deep depreciation in yen, which broke the 100-per-dollar mark, despite of the unclear long-term benefits. The recent market confidence has been lifted, while the market expects the country’s Q1 GDP with optimism.

Although the unstable trend in April, May has some positive news from the panel industry. The two Taiwanese leaders, AUO and Innolux, revealed the Q1 financial results, as the former has swung from losses to profits and the later has ended its 10 quarters of consecutive losses. Sony’s yearly financial performance has showed the first gain for the last five years, suggesting the manufacturing bounced back from the bottom and the cost would drop with the yen drop. However, looking ahead to Q3, the panel industry should be regarded with a neutral attitude mainly because China’s energy saving subsidy policy announced on Jun 1st 2012 comes to the end in May, and the market returns to the fundamentals. According to WitsView’s survey, the panel price continues to drop in the second half of May and is hard to recover in the short-term as supply surges and demand eases. When entering H2’13, if the panel industry can remain prosperous is worth cautious observations.

Remark:Please be kindly reminded that MCI data has revised as the weighted ratio changed by Q1 2013 financial result.

More detailed analysis is provided to WitsView Intelligence members. Interested in being Intelligence members? Contact us! mkt@witsview.com