Unclear global economic outlook, pane price competition intensifies after May 1st

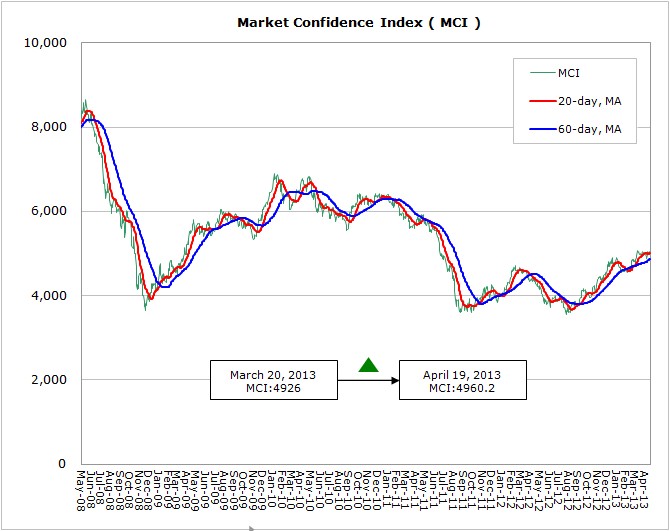

According to WitsView’s latest data, from March 20th to April 19th, MCI surged 34.2 points from 4926 points to 4960.2 points. Recently, MCI swings between gains and losses, although it shows small increase, market confidence remains unstable. In view of global macroeconomics, the U.S. PMI came to 51.3 in March, dropping 2.9 points from 54.2 in the previous month. It has been expanding for the consecutive fourth month, but the gauge fell short of market’s expectations. But in view of the quarterly growth, the U.S. economic performance in Q1 2013 was indeed stronger than that in Q4 last year with export orders and employment rate at a record high for recent years. At the current stage, the deficit-cutting mechanism hasn’t seen significant effect, and the recent terroristic attack has brought uncertainties to the U.S. economic recovery.

In Europe, the situation was very sluggish. The March PMI in the euro zone fell 1.1 points to 46.8 and reached the three-month low, and the economic contraction was deeper than experts have projected. As the economic driver of the single currency area, Germany is not exempt from shrinking growth. Based on the report issued by the German Council of Economic Experts (GCEE), the 2013 economic forecast for Germany will only attain 0.3%, lower than 0.8% last year. The deposit tax imposed by the Cypriot government last month caused a run on deposit and ended up with a bailout, indicating the concern on the European sovereign-debt crisis remains, and consumer and investor confidence is weakened again.

China’s PMI in March grew 0.8 point to 50.9, suggesting the manufacturing was expanding, but at a slower pace. On the other hand, China National Bureau of Statistics has released the Q1 GDP which declined 0.2% to 7.7% from the previous quarter. But compared with the U.S. and Europe, the Chinese economy is still on a tepid and positive path. The recent depreciation in Japanese yen has prompted the dollar/yen exchange rate to approach the 100 benchmark. With the improving export, Japan seems to faces stronger import cost pressure stirred by dropping yen, and the Japanese economic recovery is still unknown.

From the perspective of panel industry, based on WitsView’s large-sized panel shipment survey, the March large-sized panel shipment surged 17.1% MoM amid the lower basis period in February. Looking ahead to April, as the demand for May 1st in China wanes, the panel shipment enters a period of correction, and the demands in Europe and Japan stumble, the Q1 global LCD TV brands’ shipment will only reach 45.7 million units, dropping 26% QoQ, according to WitsView’s estimates. Based on our observations, after May and before the peak season in Q3, the panel demand and supply will still see fluctuations. As Korean won may closely follow the Japanese yen and rapidly drop, the panel price competition will start to intensify in Q2, and the market movement will depend on strategies adopted by panel makers.

More detailed analysis is provided to WitsView Intelligence members. Interested in being Intelligence members? Contact us! mkt@witsview.com