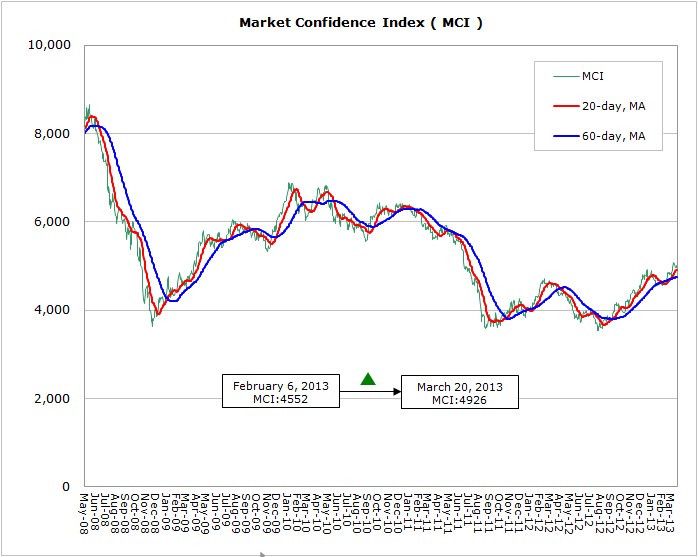

According to WitsView’s latest data, MCI has rebounded 374 points from 4552 points to 4926 points from Feb. 6th to Mar. 20th. It suggests that the market was not dragged down by the slow season in January and February, and MCI bounced strongly. In view of economic conditions in major nations, the series of economic data released by the U.S. indicated signs of economic recovery, including the February retail sales showing the most growth in five months and manufacturing PMI surging from 53.1 in January to 54.2 in February, revealing the better-than-expected industrial performance. In addition, the unemployment rate in February dropped to the lowest in four years to 7.7%, and the U.S consumer spending is expected to strengthen and lift the end demands. However, whether the automatic deficit- cutting mechanism will trim consumers’ spending is worth observations. In China, February PMI declined to 50.4 on the Lunar New Year holidays and the softening oversea demand, but the figure has remained above the 50 line for four consecutive months that divides expansion from contraction, clearly indicating the economic momentum stayed stable and continuous. The market confidence will be supported with the May 1st holidays and the energy-saving subsidy policy as the two favorable drivers.

The euro zone may also be out of the woods and sees recovery. According to Eurostat, the trade deficit in the euro zone dropped 5.2 billion Euros in January from the same period last year, and the business activities heated up in the member states that have received bailout. Japanese yen continues to slide, although Japanese officials have revised up the economic outlook and announced to join the TPP (Trans-Pacific Partnership) trade negotiations, the long-term economic condition remains to be watched cautiously. As the panel industry is supported by the gradually improving macro economy, the March large-sized panel shipment will grow 17.5 % MoM, and the LCD TV sales during the Lunar New Year holidays in China surged 9.4% YoY, according to WitsView’s reports. Chinese and Taiwanese panel makers maintain the optimistic attitude toward the pre-May 1st demand in China, and the LCD TV utilization stays at a high level. Based on our recent observations on the panel price trend, the panel prices are still pressured, and the Q2 will show uncertainties. Besides, if the economic recovery can sustain in the long term is to be observed.

More detailed analysis is provided to WitsView Intelligence members. Interested in being Intelligence members? Contact us! mkt@witsview.com