WitsView: The heated-up panel shipment after August will support the stability of panel prices

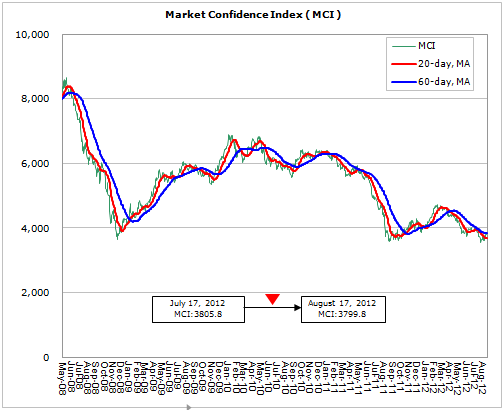

According to the latest statistics provided by WitsView, the MCI has dropped from 3805.8 to 3799.8 by 6 points during 7/17~8/17. The MCI actually dropped below 3600 points at one time before bouncing back to the creditable quarter line indicating weak market confidence. The growth of US industrial production statistics has reached a new 3-month height in July showing a gradually recovering US economy. However, the Purchasing Manager’s Index (PMI) announced by Chinese officials in July has dropped to a lower-than-expected 50.1. This is an indication that the overall economy has not significantly recovered, and the panel industry remains under the influence of global economic downturn and weak end market demand.

With the production line and technology conversion during the first half of the year, plus the cautious and effective control over production capacity, the Q2 financial statements have indicated the gradually improved profit losses among panel makers. However, the market has been expecting a market boost in Q3 based on National Day Holidays and Energy Saving Product People’s Benefitting Policy in China and the demand of stocking in advance for yearend hot seasons in Europe and US. If the panel makers can continue to support the panel prices in Q3 with effective control over production capacity and constant cost reduction, there is still a chance for panel makers to come up with a profit turnaround.

Remark: Due to the fact that China has included the panel industry as one of major focuses in terms of national development, Chinese panel maker BOE has become one of the global top panel suppliers. Therefore, starting from 3Q11, we have included BOE in the MCI index. After the adjustment on July 17, the MCI index is 3805.8.

More detailed analysis is provided to WitsView Intelligence members. Interested in being Intelligence members? Contact us! mkt@witsview.com